On the 23rd and 24th of March, the Palm and Lauric Oils Price Outlook Conference 2021 was held, traditionally held in Kuala Lumpur, Malaysia, for more than 30 years, but this year, due to the pandemic, it was presented online. This is one of the most relevant events in the world in this segment, the focus of this conference is to present the trends, perspectives and opportunities in the palm, lauric, special oils, biodiesel and oleochemicals markets.

The 2020 COVID recession is the biggest the world has seen since World War II. Currently, all countries are experiencing uncertainty and speculation. According to the talks presented at the conference, the collective opinion is that the solution to the current scenario would be mass vaccination, as once 70-80% of the population becomes immune, the pandemic would become “controlled” and recovery would begin. would start.

2021 started with slight improvements in some areas, however, it is believed that the recovery will last for a few years, mainly due to the widespread unemployment that the pandemic caused. Companies closing, banks losing profits and closing credit lines from producers, for example, caused price volatility in the commodities market to reach historic levels.

Palma and Lauricos

Palm oil remains essential to Malaysia's economy and the most produced oil in the world. Its production makes up 41% of the world's total oilseed production and will be even more relevant in the coming years. Of the main crops, it is the most profitable production in terms of investment x planted area, using 11% less land than other competitors to produce the same amount of oil.

2020 was a very volatile year for this segment. At the beginning of the pandemic, with market uncertainty, there was a drop in prices, but it quickly became a year with the highest prices in history. It is believed that 2021 will probably remain the same in terms of price, however experts at the conference mentioned that the palm market must take into consideration 3 essential themes:

Labor: The work in planting and cultivating Palma is mostly manual, with the worsening of the spread of COVID and the closure of borders, producing countries were unable to import the workforce needed for plantations, which ended up causing, among other factors, a decrease in offer.

Quality and technology: In recent years, the palm market has been suffering retaliation due to contaminants, but today there are already processes that guarantee the control of 3MCPD, Glycidol and MOSH/MOAH Minerals. This research continues to advance, as regulations in many countries become more stringent every year when it comes to food safety.

Sustainability: 40% of palm production in the world comes from the combination of small producers who hardly have any certification or rigorous quality control. It was commented that there should be subsidies that help these producers reach the levels of traceability that large refineries need. This work is already underway, with certifying bodies such as RSPO.

In such a delicate moment in terms of production, stocks and prices, the scenario should improve in Q3 and Q4 this year, where a recovery of 3.2 million tons in world production is estimated, with Indonesia obviously being the precursor to this event. .

In the Lauricos market, production in 2020 was lower than expected, especially in Côco, where the market was greatly affected by lockdown issues, typhoons and floods, with the price doubling compared to previous months, and the variation for PKO, reaching the highest numbers in history, $325/MT. The reception of purchases in Indonesia and the Philippines remains limited at the beginning of the year, but an improvement is expected in the 2nd half of the year, where Palm Kernel production will also increase, starting a recovery in stocks.

Biodiesel and Oleochemicals

Although the Biodiesel market has increased demands, exports have fallen drastically. Producing countries are keeping products on the local market. Indonesia, for example, a global reference in Biodiesel production, had an increase of 24% in the consumption of palm oil for production (due to the implementation of B30). However, its exports fell by more than 80%, leaving the entire volume in the domestic market. Something similar happens in Malaysia, however they are in the B20. These high mandates serve to fill the hole left by the blockade of Palm Oil in European Biodiesel.

To give you an idea, 80% of the volume of Palm Methyl Ester (PME) exports from Malaysia and Indonesia go to Europe. By the end of 2030, they intend to ban 100% and thereby increase demands for waste oils (UCO, POME, PAO, PFAD, CNSL) and make room for HVO, a renewable diesel, which presents itself as one of the alternatives promising for an energy transition, as it is a renewable fuel produced only from vegetable and waste oils. It is estimated that by 2025 its use will triple, supported by the media campaign in the EU against palm for fuel.

In the oleochemicals market, the increase in vegetable oil prices tends to be a major concern for this sector, as a large part of the cost of oleochemicals is in raw materials. It is believed that it was one of the sectors most affected by the current freight crisis as it is not just something in the maritime sector, but in all modes. In addition to shipping being 3 times more expensive than at the same time last year, there is still great difficulty in finding space on ships. For this market it was an inconvenience, considering that shipping exceeded the price of the product, which already has low added value. As a result, many suppliers are not exporting, thus maintaining the local market, which has the consequence of increasing stocks as local demand does not absorb all production.

Oleochemical products are Bio-Friendly, which is why this market was not so at the mercy of this period of crisis. Hygiene and cleaning industries, such as P&G, for example, saw their shares increase in value, as with the pandemic the population began to consume more cleaning products. It is believed that this demand will continue even after this period. For the oleochemicals market outlook for 2021, the increase in alcohol gel, disinfectant wipes and all cleaning products is expected to continue.

{module Form RD}

For the fatty acids segment, demand is also on the rise, especially in cleaning areas, but competition with tallow and other products of palm origin end up taking away its space, but it is still a promising market. The animal nutrition sector remains robust and is also picking up much of this volume. In addition to the high logistical values, the main problems for fatty acids today are the costs and competition for the use of raw materials: palm, palm kernel, coconut, tallow, soy and canola.

The demand for fatty acids has always closely followed the economy. As for glycerin, global production is steady, as glycerin is a byproduct of biodiesel production. Good global production favors consumption demands in the Chinese market, which in short is one of the main destinations for Glycerin, but due to the complicated shipping situation, this becomes a very challenging task. In the long term, there is a concern about the replacement of biodiesel and the supply of HVO (renewable biodiesel) because, if it actually occurs, the process will not generate glycerin as its by-product, therefore, the question is: will we need synthetic glycerin again?

In terms of fatty alcohols, due to the need for cleaning caused by the pandemic, the demand outlook is good. The market for C16 and C10 is very strong and business for C1618 is much firmer than normal. However, the high price levels of raw materials have increased the prices of fatty alcohols, which were previously traded at USD 1,214/MT are now around USD 2,000/MT. Furthermore, the sector suffers from transport problems causing a shortage of ships and containers in several ports, affecting the supply chain.

Some oleochemical plants are cutting their production and some customers are looking for alternative products. Surfactant technology is under pressure, and in the personal care sector the search is on for alternatives to sulfate alcohol chemicals. Climate change is impacting the production of palm fruits and other crops, affecting businesses. This influences synthetic alcohol, which is about 25-30% of the total alcohol supply, and this would be a bonanza for the natural alcohols business, which is likely to gain momentum. Consumers are now responding more to environmental needs and bio-friendly materials such as oleochemicals. As presented at the Conference: “Cleaning has soared, a new normal.”

Soft Oils

When analyzing the pre-pandemic scenario, vegetable oils were already rising, due to the increase in biofuel mandates, Malaysia and Indonesia. With the pandemic and the beginning of lockdown, for the first time the food market did not increase its demand, on the other hand there was exponential growth in the fuel industry. To give you an idea of the tremendous appreciation of vegetable oils on the market, in the last 5 years, prices have already risen by around 70%. And in the last 12 months alone, these values have more than doubled, especially in special oils.

Soybean oil accounts for 25% of global production and its demand is extremely high, mainly due to the Biodiesel market. What will influence the price in the coming months will be the performance of the crops and Chinese demand. Regarding the harvests in Brazil and Argentina, there is still speculation in the numbers due to climate concerns, but in general, Brazilian production is estimated at 131M and Argentina at 44M tons. If this happens, China should maintain a high volume of imports, which in recent months has already been a record. However, they should be concentrated in the first half and be lower in the second.

In addition to grains, China is also expected to increase its soybean oil import numbers. With the reduction in pig farming in the local market, the surplus volume of soybean meal is very high, so it is expected that they will process less grain and focus on importing oil.

With China less active in importing soybeans in the second half of the year and the United States in full harvest, a possible increase in North American stocks can be expected, which are currently among the lowest in the last 7 years. Worldwide, a greater demand for oil is expected this year, which is why the forecast is that global soybean crushing will increase between 10-11 M tons more than in 2020.

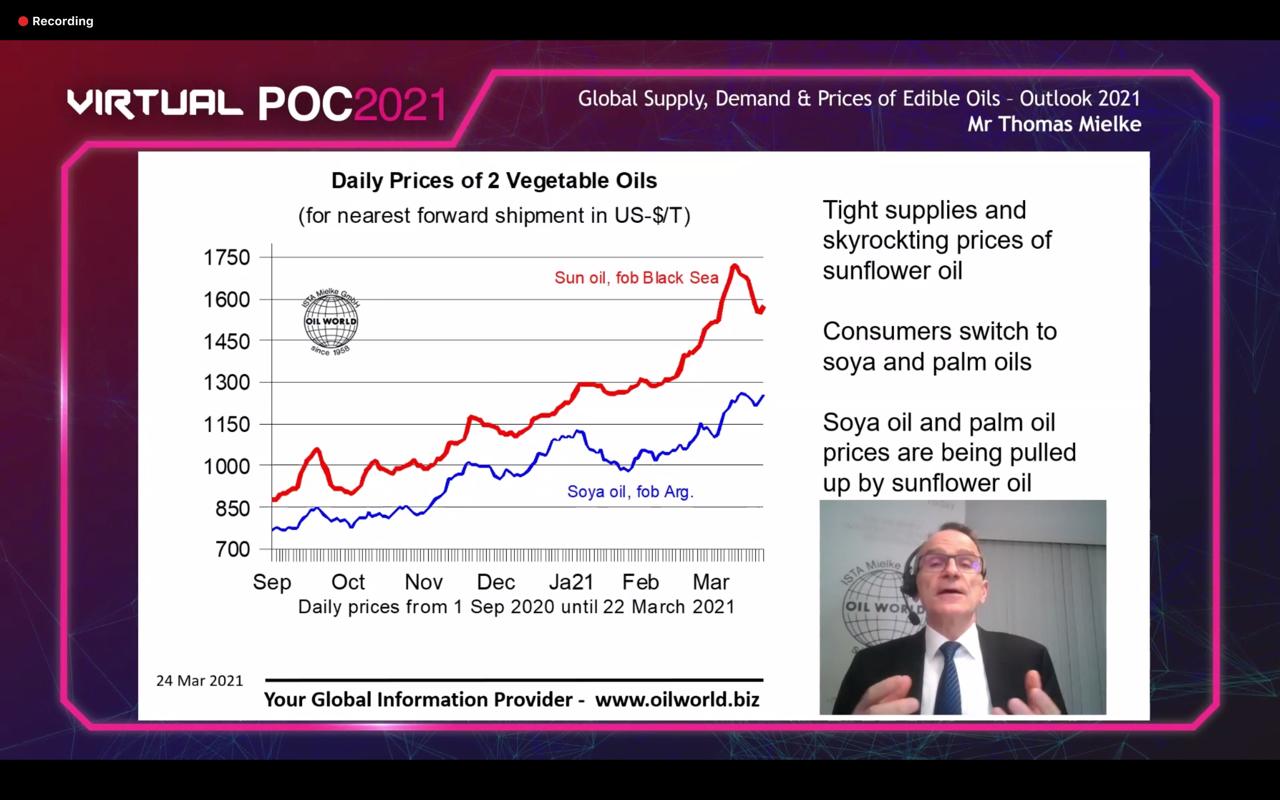

In relation to sunflower oil, in 2020 it played a relevant role as its price increase impacted all other oils. When palm and soybean oil began to rise and became scarce on the market, many buyers switched to sunflower, causing greater demand. Then, the Black Sea harvest, which concentrates world production of this item, suffered a decline due to weather conditions. This entire scenario led sunflower to its highest price in the last 5 years.

To get a clearer idea of this scenario, in October/November 2020 production started, with delay, as normally in September we can already see several shipments taking place. Although the planted area grew compared to the previous harvest, the seed yield was much lower than expected. This is mainly due to bad weather during planting, leaving the soil dry to absorb all the necessary nutrients. With production damaged, we could only expect a loss in global sunflower oil production, which remains at approximately 5 million tons to this day.

With the harvest delayed and prices rising, buyers were quick to set prices. Several operations from November to March were outlined, mainly with China and India as the main buyers. In turn, producing countries applied new export taxes, which helped keep prices high.

In March, it was expected that with the arrival of the Latin American harvest, prices would drop, placing more product on the market. Unfortunately, the numbers were not positive either, and helped to keep the price of sunflower oil high, always with great volatility.

As a way to overcome the large price variation, consumers replace their need for other oils, such as canola, soy and palm. Black Sea sales forecasts are not fulfilled; Several defaults occur, as they are unable to maintain the prices negotiated in advance, generating even more instability in this market, so much so that it was the only product in which none of the experts dared to give price forecasts for Q4.

Although other special oils have not had much focus, in the opinion of our experts:

- Corn Oil: The rise in the price of corn oil is a constant that, added to the low supply and high demand, the market balance disappears. With most players positioning themselves with future offers, and buyers fearing a break in the supply chain, they are firming their demands and guaranteeing their volumes. The focus will be on the 21/22 US corn harvest, where the weather factor will be essential in determining the course of prices.

- Peanut Oil: This product was also impacted by the rise in prices of other vegetable oils, reaching its highest level since 2016, but driven mainly by the particular situation in exporting countries, in addition to strong Chinese demand. It is considered that the price may undergo corrections this year, but should still remain at high levels, depending, of course, on the progress and results of the Chinese harvest, which corresponds to more than 40% of world production.

- Canola Oil: Like the rest of the special oils, it suffered a large increase in prices, but it was not as sharp as other oils. In the last two years, China was its biggest importer and as a result, it ended up depleting the local market and making Canada become an importing country for the first time. Even with the good European harvest, the price of canola oil should remain firm, as many sunflower buyers are replacing their demand with canola, as already mentioned.

In conclusion, our experts agree with the opinion of Thomas Mielke and James Fry, that if vegetable oils have not yet reached their peak, they are very close to it. They should remain at this level until the end of Q2 and there is a slight tendency for prices to decline in the second half of the year, however, even with this decline, prices should remain high throughout the year. The determining factors that will dictate which direction the market will follow will be: The US soybean harvest (June and July), East Asian palm and Black Sea sunflower (September, October). Furthermore, it is worth monitoring the vaccination rate in the world, the level of unemployment and the pace of economic recovery.

Per: Tiago Vicente, Michel Malvasi, Renan Fernandes, Muriel Malvasi, Laura Pereira, Zainab Alhamwi, Melinda Rodrigues and Thiago Prianti | Aboissa Commodity Brokers

Did you like it and want to know more about the market? Register to receive more information directly to your email or contact contact with one of our experts.

Read too:

")

")

")